of CO2 emissions per year

risks.

The following risks may be materially relevant but may not always be adequately captured by the summary risk indicator and may cause additional loss: Operational risk and risks related to asset safekeeping, Model risk and Financial, economic, regulatory and political risks. Sustainability risks may lead to a significant deterioration in the financial profile, profitability or reputation of an underlying investment and may therefore have a significant impact on its market price or liquidity. The environmental, social, and governance (“ESG”) considerations discussed herein may affect an investment team’s decision to invest in certain companies or industries from time to time. Results may differ from portfolios that do not apply similar ESG considerations to their investment process.

Silvercrest Equity

Decarbonise, diversify and drive the transition

While the industry has started to understand the urgency around decarbonisation, we believe many of the solutions available in the market are simplistic, do not sufficiently address the problem and, in some cases, significantly increase the risks and biases within portfolios. Investors need to re-think their approach to net zero.

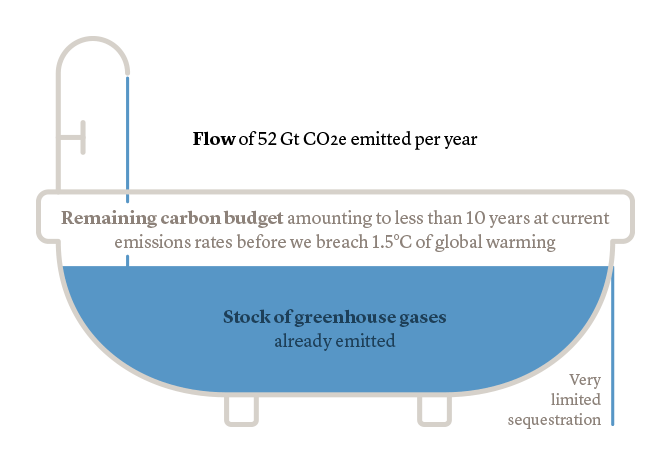

52 bntons

Zeroemissions

required by 2050 to keep global warming

within 1.5C degrees

50%reduction

of greenhouse gas emissions

by 2030

investing with a true net-zero focus.

the nature of the climate problem.

Bill Gates on climate change.

“The climate is like a bathtub that’s slowly filling up with water. Even if we slow the flow of water to a trickle, the tub will eventually overflow.”

climate investment challenges.

why us?

Combining the strengths of our science-based, forward-looking sustainability research team and well-established systematic equities team, we aim to deliver a true net-zero-aligned portfolio.

We do this by investing in the leaders of the climate transition within each industry, while reducing exposure to its laggards. Rather than artificially limiting our exposure to the low-carbon subset of our economy, our approach also allows us to address and engage with the most climate-relevant sectors.

This broad approach recognises that the greatest positive impact on decarbonisation will come from companies that are currently high emitters, and that have the commercial need and financial resources to transition to a much lower level of emissions in the future.

We aim to deliver on three parameters:

|

Redeployment of capital |

|

Reducing the transition risk for investors, thus generating risk-adjusted returns as our global economy evolves. |

|

Rising awareness |

|

Offering an investment opportunity in line with the climate goal to limit GHGs and consumer demand. |

|

Market forces |

|

New targets and regulations are increasingly focussed on circularity, nature, equality and net zero. Technological innovation and economies of scale are driving down costs |

our strategy.

Our Silvercrest equity funds aim to manage transitional, physical and liability risks while capturing opportunities among companies aligning to net zero.

A low-tracking error approach gives our Global and European equity strategies the ability to tap into a broad opportunity set, thereby:

- Reducing carbon footprints

- Managing climate transition risk

- Offering a route for investing across the entire economy

- Accelerating the climate transition

- Maintaining portfolio diversification

- Targeting climate growth opportunities

investment philosophy.

“Carbon footprints alone do not tell us the full picture of climate risks in a portfolio. We believe that maintaining a diversified portfolio that identifies companies on a strong decarbonisation path, irrespective of sector, will help accelerate the transition to net zero and provide compelling returns for investors.” – Nicolas Mieszkalski, Portfolio Manager.

looking for ‘ice cubes’. avoiding ‘burning logs’.

Many companies in emissions-intensive industries – like steel, cement and energy – are viable opportunities for our Silvercrest portfolio. Why?

Firms in these hard-to-abate sectors that are rapidly cutting emissions are essential to reaching net zero. Because they are helping to cool the economy, we call them ‘ice cubes’. In contrast, polluting companies that are failing to take action are ‘burning logs’.

By seeking opportunities among ice cubes, we aim to support impactful decarbonisation while potentially benefiting from the growth prospects of companies aligning to the net-zero transition.

Finding leaders and avoiding laggards.